Difference Between LOS and LMS in the Lending Lifecycle

Loan Origination System (LOS) and Loan Management System (LMS) are two core components of modern lending technology. Yet, they are frequently misunderstood and sometimes treated as interchangeable. This confusion often surfaces during platform evaluations, system migrations or when operational bottlenecks begin to appear. In reality, LOS and LMS serve distinct purposes at different stages of the lending lifecycle. Understanding the difference between them is essential for building scalable, compliant and efficient lending operations.

Why LOS and LMS are often confused

Both LOS and LMS deal with loans, which makes it easy to assume they address the same problems. In early-stage lending setups, a single system-or even spreadsheets-may be stretched to handle both origination and servicing, reinforcing this misconception.

As lending volume grows, the lack of clarity starts to show up as:

-

Manual coordination between teams

-

Delays in disbursal or servicing

-

Reconciliation and reporting challenges

-

Difficulty scaling partner or marketplace channels

These issues are usually not people problems - they are system role clarity problems.

What is a Loan Origination System (LOS)?

A Loan Origination System (LOS) manages all activities that occur before a loan is disbursed. Its primary role is to support risk assessment and credit decisioning in a structured and compliant manner.

Typical LOS responsibilities include:

-

Loan application capture

-

Document collection and verification

-

Identity checks and KYC

-

Credit assessment and underwriting

-

Approval workflows and offer generation

LOS is primarily used by sales, credit, and underwriting teams. Once a loan is approved and ready for disbursal, the LOS typically hands off the loan to downstream systems.

What is a Loan Management System (LMS)?

A Loan Management System (LMS) takes over after loan disbursal and manages the loan throughout its active lifecycle.

Typical LMS responsibilities include:

-

Repayment schedule creation

-

EMI collection and posting

-

Interest, fees and penalty calculations

-

Delinquency and collections workflows

-

Customer account servicing

-

Ledger maintenance and reconciliation

-

Portfolio and regulatory reporting

LMS is primarily used by operations, finance, collections and compliance teams and is designed to handle long-term, transaction-heavy workflows.

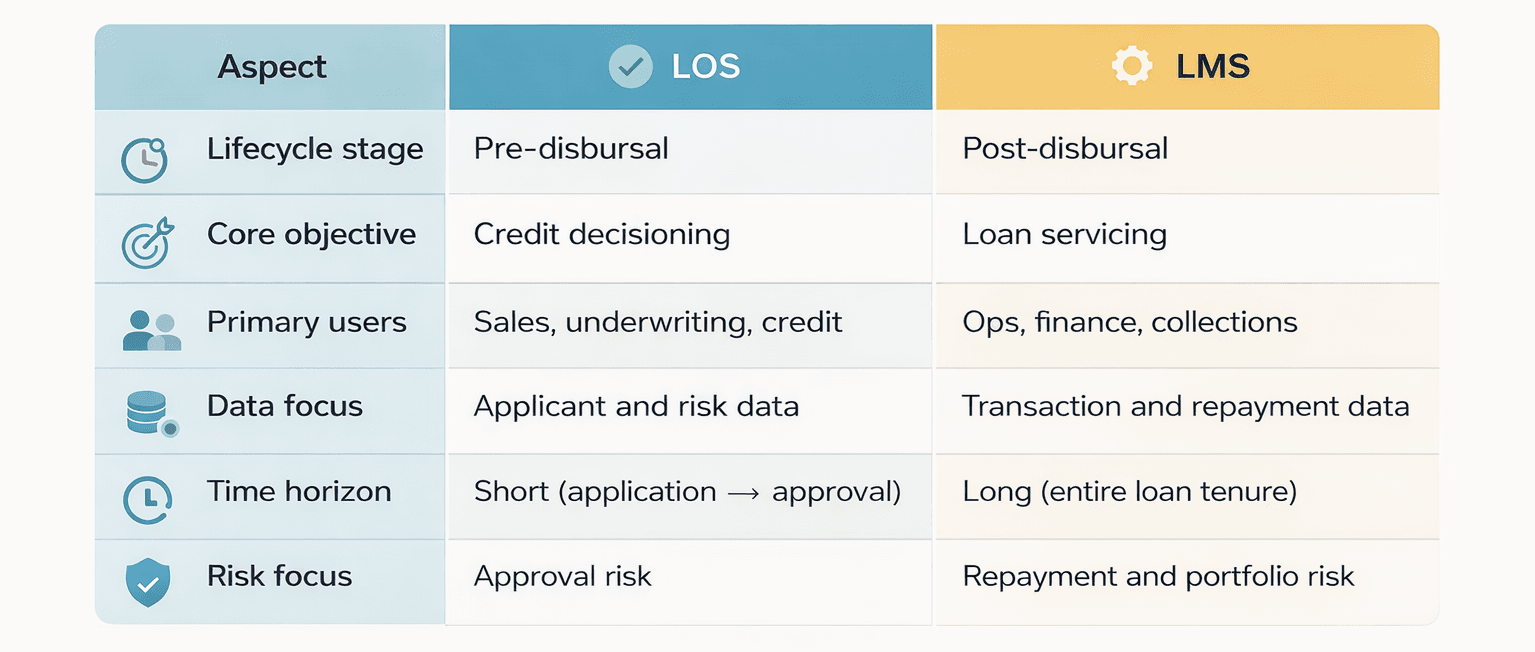

Difference between LOS and LMS

LOS is focused on the pre-disbursal phase, where the lender’s priority is to assess risk and make accurate credit decisions. It supports short-cycle workflows such as application intake, verification, underwriting and approval. Once a loan is sanctioned and disbursed, the LOS has largely completed its role.

LMS takes over in the post-disbursal phase, managing the loan over its full tenure. Its focus shifts to execution and control - handling repayments, servicing customer accounts, managing delinquencies and maintaining accounting and regulatory accuracy over time.

LOS works with applicant and risk data used to decide whether a loan should be issued, while LMS works with transactional and repayment data that evolves continuously after disbursal. Because these systems are optimised for different time horizons and risk types, they are not interchangeable.

Why LOS and LMS are not interchangeable

Problems arise when one system is expected to handle responsibilities outside its intended scope.

Common scenarios include:

-

Using an LOS to manage EMIs, collections or accounting

-

Using an LMS to capture applications and perform underwriting

-

Relying on spreadsheets to bridge gaps between systems

These approaches may work temporarily but often result in:

-

Increased manual effort

-

Slower turnaround times

-

Higher reconciliation workload

-

Compliance and audit risks

As scale increases, these gaps become increasingly difficult to manage.

How modern lending stacks are actually designed

Most mature lending architectures follow a modular approach:

- LOS for origination and decisioning

- LMS for servicing and accounting

- A workflow or orchestration layer connecting the two

This orchestration layer is responsible for:

-

Managing state transitions between systems

-

Coordinating lead and loan movement

-

Enforcing routing logic and operational SLAs

-

Normalising data between systems

-

Providing end-to-end traceability and audit logs

Rather than replacing LOS or LMS, orchestration ensures they work together reliably as lending operations grow in complexity.

Common mistakes lenders make

Some recurring mistakes seen across the industry include:

-

Selecting systems based on overlapping features instead of lifecycle fit

-

Overloading LOS or LMS to avoid adding supporting infrastructure

-

Ignoring orchestration and integration until problems become visible

-

Treating partner or marketplace workflows as edge cases

These decisions often delay operational maturity and create long-term scalability issues.

Why workflow orchestration becomes critical at scale

As lending operations expand across products, geographies, and partner channels, coordination becomes the real challenge.

Workflow orchestration layers help by:

-

Standardising intake across multiple channels

-

Managing system handoffs without manual intervention

-

Enforcing consistent operational rules

-

Reducing reconciliation effort through structured events

-

Maintaining audit-ready visibility across the loan lifecycle

This layer turns disconnected systems into a cohesive operating model, enabling predictable execution even as volume increases.

Choose systems by lifecycle, not by labels

LOS and LMS are both essential, but they are designed for different stages of the lending journey. A scalable lending operation depends on:

-

Clear separation between origination and servicing

-

Reliable system integration

-

Workflow coordination that does not rely on manual oversight

Choosing systems based on where they fit in the lending lifecycle - rather than treating them as interchangeable - is what ultimately determines operational stability and growth readiness.

FAQs

- What is the main difference between LOS and LMS?

LOS handles pre-disbursal activities such as application processing and underwriting, while LMS manages post-disbursal activities like repayments and collections.

- Can a lender operate with only one system?

Small setups sometimes do, but as volume and complexity increase, this often leads to operational and reconciliation challenges.

- Do LOS and LMS need to be integrated?

Yes. Integration ensures consistent data flow, accurate state transitions, and smooth operations across the loan lifecycle.

- What role does workflow orchestration play?

It connects LOS and LMS, managing routing, state changes, exception handling, and operational visibility.

- Where do partner and marketplace channels fit?

- Partner-led channels increase the need for orchestration due to higher coordination, routing, and reconciliation requirements.